Honeywell Valuation Outlook as Aerospace Spinoff Reshapes Strategy

AutoControl GlobalAutoControl Global January 27, 2026Honeywell International Valuation Gains Attention as Aerospace Spinoff Advances

Leadership Changes Renew Market Focus on Honeywell

Honeywell International has returned to investor focus after announcing Josh Jepsen as CFO of its planned Honeywell Aerospace spinoff.

Jepsen previously served as finance chief at Deere & Co., bringing strong operational finance experience.

Moreover, this leadership update aligns with a recent JPMorgan upgrade, reinforcing market confidence.

Recent Share Price Performance Signals Momentum

Honeywell shares currently trade around USD 221.

Over the past 30 days, the stock delivered a double-digit return, while year-to-date performance remains solid.

Therefore, recent gains appear to build on a steady long-term trend rather than short-term speculation.

Valuation Context Within the Industrial Automation Landscape

At current levels, Honeywell trades below one intrinsic value estimate near USD 236.

This suggests a moderate undervaluation, even after recent price appreciation.

However, investors must consider whether future growth expectations already influence the stock.

From an industrial automation perspective, Honeywell benefits from diversified exposure.

Its portfolio spans factory automation, control systems, aerospace, and building technologies.

As a result, earnings stability often exceeds that of more narrowly focused PLC or DCS suppliers.

Portfolio Reshaping and Strategic Acquisitions

Honeywell continues to refine its business mix through acquisitions like Sundyne.

These bolt-on moves expand process automation and flow control capabilities.

In addition, they support margin improvement by strengthening high-value industrial solutions.

The company’s local-for-local manufacturing strategy also reduces tariff exposure.

This approach improves supply chain resilience across global automation projects.

Therefore, Honeywell maintains competitiveness in both mature and emerging markets.

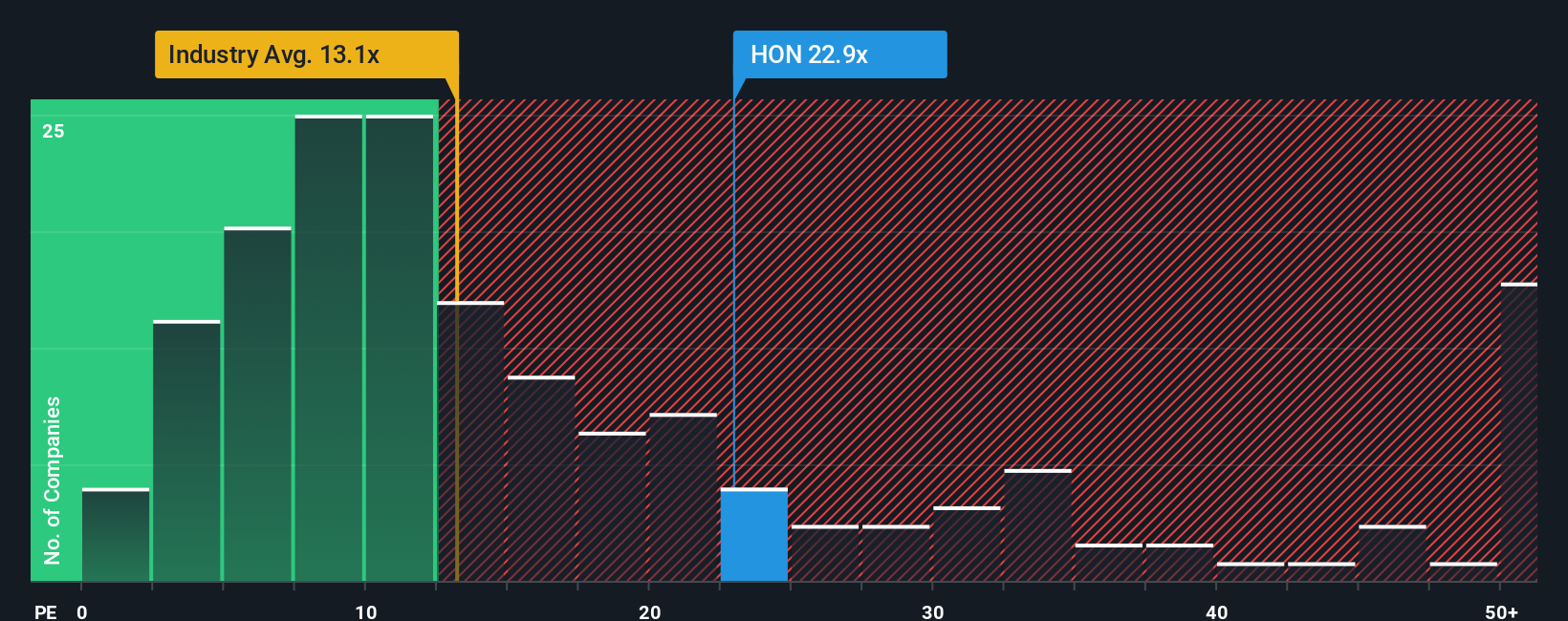

Earnings Expectations and Multiple Expansion Risk

Honeywell’s current P/E multiple stands above the global industrial average.

However, it remains below several aerospace and automation peers.

As a result, valuation risk depends on execution during the planned three-way separation.

In my experience with large-scale control systems deployments, organizational clarity matters.

Clear segment focus often improves capital allocation and R&D efficiency.

If executed well, the spinoff could justify a higher long-term valuation multiple.

Risks That Could Disrupt the Valuation Narrative

Despite positive signals, execution risk remains material.

Separating aerospace, automation, and advanced materials adds operational complexity.

Softer revenue growth or delayed synergies could pressure margins.

Investors should also monitor automation demand cycles.

Factory automation and PLC investments tend to slow during industrial downturns.

Therefore, macro conditions still influence Honeywell’s near-term performance.

Industrial Automation Relevance and Practical Insight

From an engineering standpoint, Honeywell’s strength lies in system integration.

Its DCS platforms, safety systems, and industrial software support complex facilities.

These capabilities create long-term customer lock-in across energy and manufacturing sectors.

I have seen Honeywell control systems perform reliably in high-availability environments.

Such operational trust supports recurring service and lifecycle revenue.

This practical advantage often receives less attention than headline valuation metrics.

Application Scenarios and Solution Outlook

Honeywell solutions commonly appear in refineries, power plants, and smart factories.

Integrated PLC, DCS, and safety architectures reduce downtime and simplify maintenance.

As digitalization accelerates, demand for unified control systems should remain durable.

Conclusion: Balanced Opportunity With Execution Dependence

Honeywell’s valuation story combines industrial automation stability with aerospace optionality.

Leadership changes and portfolio reshaping add credibility to future growth assumptions.

However, sustained upside depends on disciplined execution and market conditions.